Do You Automatically Get a CIBIL Score at 18?

Shocking CIBIL Myth EXPOSED: Think turning 18 gifts you a score? WRONG! Unlock the hidden truth delaying millions’ dreams—cars, homes, startups. What 90% get wrong (and how to fix FAST). Will YOU build 800+ by 25? Dive in before banks slam doors!

Turning 18 marks adulthood in India – the age to vote, drive, and sign contracts. But does it also mean an automatic CIBIL score? This common belief spreads fast on social media and forums, especially among excited teens planning their financial futures. The short answer is no. A CIBIL score isn’t handed out like a birthday gift upon hitting 18. It forms only after real credit activity. This post dives deep into why, how scores actually work in India, and actionable steps for young adults to build strong credit from scratch.

Understanding CIBIL Scores

CIBIL, or Credit Information Bureau (India) Limited, leads as India’s primary credit bureau, compiling data from banks and financial institutions to assess creditworthiness. The score ranges from 300 to 900, where 750 or higher indicates low risk to lenders, facilitating better loan terms and interest rates. Without any credit history, no score exists, as CIBIL requires reported activity like loans or credit cards before generating one.

CIBIL does not automatically assign profiles or scores simply upon reaching 18 years of age. Lenders report credit usage—typically after 6 months of consistent data—triggering score creation. This leaves many young adults “score-less,” complicating access to initial credit products despite legal eligibility at 18.

Over 500 million Indian adults lack formal credit histories, according to RBI estimates, hitting rural youth and fresh graduates hardest. The misconception of automatic scores stems from contrasts with U.S. models like FICO, which may provide starter scores, whereas India’s system demands proven activity for accuracy and reliability.

Why the “Automatic at 18” Myth Thrives

- Viral Social Media Claims: Platforms like TikTok, Instagram Reels, and Reddit (e.g., r/CreditCardsIndia threads) spread quick claims like “Turn 18, get instant CIBIL!” These short videos prioritize engagement over accuracy, confusing viewers who assume adulthood equals credit profile.

- Misunderstanding Add-On Cards: Many cite parents adding kids to cards at 18 as “instant score,” but it requires actual usage and reporting (3-6 months) – not automatic. Forums amplify partial truths without full context.

- Cultural Emphasis on Saving: Indian families prioritize fixed deposits and gold over credit, leaving youth undereducated. Credit talk feels taboo, so first exposure via peers or ads creates myths like “legal age = score.”

- Life Milestone Assumptions: Youth encounter CIBIL during college loans, jobs, or weddings, assuming it starts at 18 like voting rights. Delayed formal finance education reinforces this.

- Unverified Online Sources: Blogs and quizzes falsely claim “government mandates CIBIL at majority,” ignoring RBI rules. Viral posts gain traction without fact-checks.

- U.S. System Confusion: Unlike FICO’s occasional starter scores, India’s RBI-mandated bureaus (CIBIL, Experian, Equifax) demand verified activity only – no auto-profiles. Cross-border content muddies waters.

- Rapid Digital Credit Rise: BNPL apps and pre-approvals make borrowing seem effortless, leading to surprise when no score appears. Lack of disclaimers fuels “it should be automatic” belief.

- Opaque Bureau Processes: RBI guidelines limit reports to lender-submitted data, but low awareness of this (no public campaigns) breeds assumptions of default creation at 18.

What Happens When You Turn 18 Financially?

Turning 18 grants legal adulthood in India, enabling independent financial products without guardians, but access hinges on KYC (Aadhaar, PAN) and often income proof. Banks verify age first, then scrutinize credit history – no score typically means denials or alternatives like secured options.

Key Eligible Products

- Bank Accounts: Full rights to zero-balance savings accounts at SBI, HDFC, or ICICI without parental consent; enables UPI and salary credits.

- Debit Cards: Issued instantly with account; no credit check needed for basic versions.

- Credit Cards (Entry-Level): Possible via secured (FD-backed like IDFC FIRST WOW Student, min ₹5,000 FD) or add-on cards; standalone like Amazon Pay ICICI often lists 18+ but practically requires 21+, income (₹15k+/month), and score >750.

- Small Personal Loans/Education Finance: Rare at 18; most lenders (Bajaj Finserv, Aditya Birla) mandate 21+ due to income/repayment risks, though gold loans or NBFC consumer loans (Home Credit) start at 18 with collateral.

Challenges Without Credit History

Eligibility exists, but no CIBIL score triggers rejections for unsecured products, pushing high-interest secured loans (12-20% rates). Multiple inquiries harm future apps; youth often need co-signers.

Steps to Build Your First CIBIL Score

Actively build credit starting at 18 to generate your first CIBIL score within 3-12 months via lender-reported activity. Focus on one product initially, ensure timely payments (35% score weight), and keep utilization under 30%. Monitor via free annual CIBIL report.

Step 1: Open a Bank Account

Secure a zero-balance savings account at SBI, HDFC, or local co-operative banks – no guardian needed at 18. Link UPI for transactions; while not directly creating CIBIL, it establishes KYC/digital footprint for future approvals.

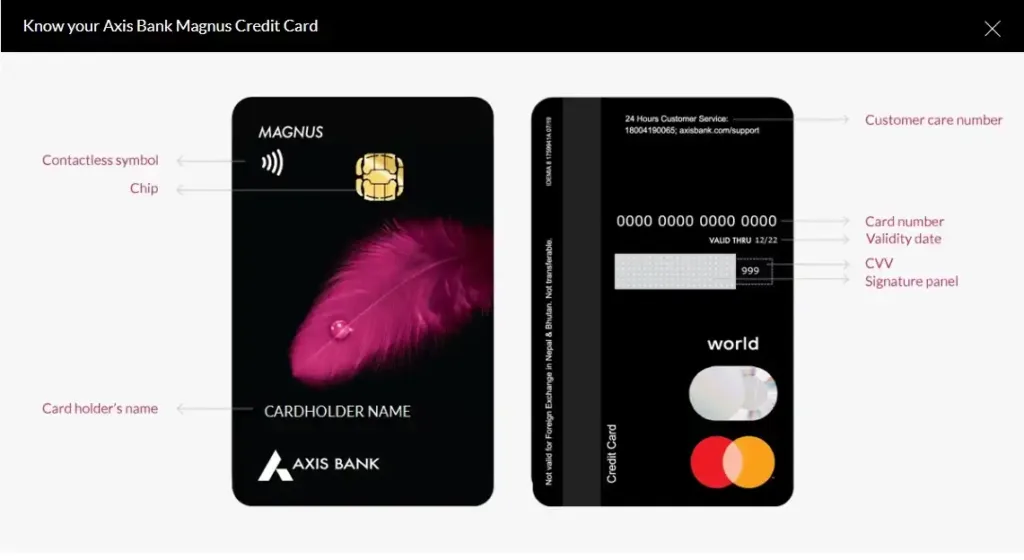

Step 2: Get an Add-On Card

Request a supplementary card from parents (e.g., Axis Magnus, HDFC Regalia, or SBI Cashback). Use responsibly (<30% limit), pay full bills on time – activity reports to your CIBIL after 3-6 months as primary user history. Parents liable, so communicate spends.

Step 3: Apply for Entry-Level Credit Cards

Target beginner-friendly options with college ID, Aadhaar, PAN:

- Amazon Pay ICICI: Lifetime free, 1-5% cashback on Amazon; prefers 21+ but 18+ via salary proof.

- Kotak 811 Dream Different: Secured on FD (₹5k+), ideal no-history starters.

- SBI SimplyCLICK: ₹499 fee, 10X rewards on online spends (Swiggy, Myntra); low-limit entry.

Odds improve with stable account; avoid multiples to prevent inquiries.

Step 4: Take Small Loans

Opt for quick reporters:

- Gold loans from Muthoot Finance (18+, collateral-based).

- Education loans via Vidya Lakshmi portal (govt-backed).

Repay EMIs on time – fastest for history (1-3 months impact). Digital loans (Olyv) also work.

Step 5: Leverage BNPL Services

Apps like LazyPay, Simpl report to CIBIL (positive if timely):

- Small buys (<₹5,000), 15-day pay.

- Opt-in for reporting; defaults hurt score badly.

Wide merchant acceptance, but treat as loans.

Monitoring Your CIBIL Progress

Track score development regularly to ensure accurate reporting and catch errors early. Access one free full credit report annually from CIBIL’s official website (cibil.com) or the MyCIBIL app – requires PAN, basic details. Paid subscriptions (₹550/quarter or ₹1,250/year) offer unlimited checks, score simulators, and alerts without impacting score (soft inquiries). Check other bureaus like Experian or Equifax similarly for complete view.

Expanded Starter Products

Use this table for quick comparison of beginner options at 18+. Security builds trust for no-history applicants; time to impact assumes perfect payments.

| Starter Product | Min Age | Security Needed | Time to Score Impact | Key Notes |

| Add-on Card | 18 | None | 3-6 months | Parent primary; your usage reports separately. |

| Secured CC (FD) | 18 | ₹5,000+ FD | 1-3 months | Kotak 811/SBI; card limit = 90% FD. |

| Gold Loan | 18 | Gold jewelry | Immediate | Muthoot; low interest, quick EMI start. |

| BNPL | 18 | None | 6 months | LazyPay/Simpl; opt-in reporting essential. |

Tips for Effective Tracking

- Monthly Routine: Log in post-statement; verify accounts, limits match.

- Dispute Errors: Online portal resolves 80% in 30 days (e.g., wrong dues).

Score Milestones: Aim 700+ first year; use apps like Cred for reminders.

Consistent monitoring prevents surprises during big apps like education loans.

Factors Shaping Your Early Score

Once your first score generates (after initial activity), it evolves based on five weighted components, updated monthly from lender reports. Maintaining 750+ early sets up low-rate loans by 21. Festivals like Diwali amplify risks via spending surges.

Detailed Components

- Payment History (35%): Core factor – on-time EMI/statement payments build trust. Never miss; set auto-debits via bank apps. Late pays (30+ days) drop score 100+ points, lingering 7 years.

- Credit Utilization (30%): Ratio of used credit to limit – target <30% (e.g., ₹3,000 limit: max ₹900). High usage (>50%) signals risk; pay mid-cycle to lower.

- Length of Credit History (15%): Average age of accounts – starts low at 18, grows with time. Patience vital; closing old cards shortens it.

- New Credit Inquiries (10%): Multiple hard pulls (loan/card apps) lower score temporarily (6-12 months). Limit to 1-2/year early.

- Credit Mix (10%): Variety (cards, loans, retail) shows versatility – add later (e.g., gold loan + card). Unsecured dominates initially.

India-Specific Tips

Diwali/ wedding spikes push utilization; pre-pay bills. Aim 750+ by 21 for housing eligibility (e.g., PMAY schemes). Rural/UP users: Prioritize EMIs over cash withdrawals.

Common Pitfalls for 18-Year-Olds

New 18-year-olds often stumble on basics, tanking nascent scores. Awareness prevents long recoveries (1-2 years).

- Over-Applying (Multiple Inquiries): 5+ apps trigger hard inquiries, dropping score 50-100 points each (lasts 6-24 months). Wait 6 months between; pre-qualify on Paisabazaar.

- High Credit Utilization: Free swiping on ₹20k card spikes ratio >50%, crashing score (e.g., 100-point drop). Pay twice monthly; stay <30%.

- Co-Signing Family Loans: You’re jointly liable – family defaults scar your report 7 years, blocking personal credit. Avoid unless stable guarantor.

- Ignoring Credit Reports: Unchecked errors (wrong PAN, duplicate accounts) persist, wrongly lowering score. Review free annual report; dispute online.

Case Study: Rohan’s Lesson

Rohan (Delhi, 19) maxed ₹20k entry card on gadgets – utilization hit 100%, score fell to 650. Recovery: Zero usage, full pays for 12 months, rebuilt to 720. Common in metros; early discipline faster fix.

Long-Term Strategy: From 18 to 30

Progress credit from 18-30 aligns with milestones: college, career, family. Early habits yield 800+ by 30 for optimal rates. Govt schemes aid underserved groups.

By Life Stage

- College Years (18-22): Focus add-on card + 1 primary (secured). Target 700+ via low utilization, timely pays. Builds base without income pressure.

- First Job (22-25): Upgrade to ₹1L+ limit cards (rewards-focused). Add personal loan for mix. Target 750+; salary account boosts eligibility.

- Marriage/Home (25-30): Diversify (mortgage pre-qualify). 800+ unlocks low-rate housing (PMAY at 28 avg age). Emergency fund covers gaps.

Government Boosts

- PMJDY Accounts: Zero-balance savings create indirect history; 6 months usage enables overdraft RuPay card, aiding formal credit entry.

- Stand-Up India: Loans ₹10L-₹1Cr for SC/ST/women greenfield ventures (18+); clean history preferred, no fixed score cutoff – boosts entrepreneurs.

Milestone Roadmap Table

| Age Milestone | Target Score | Key Actions |

| 18-20 | 700+ | Add-on + BNPL; savings account |

| 21-25 | 750+ | Primary card + small loan; job-linked |

| 26-30 | 800+ | Multiple products, low util; diversify |

Myths Busted Beyond Auto-Generation

Beyond the auto-generation falsehood, these persist due to misinformation. RBI and bureaus emphasize verified facts only.

Core Myths and Facts

- Myth: Score Starts at Birth (Even via Family): No profile auto-creates at birth or through family links. Individual activity required; inheritance/co-signing doesn’t transfer scores. Fact: Each person needs own history.

- Myth: Frequent Checks Hurt Score: Self-checks are “soft inquiries” – zero impact. Only lender “hard inquiries” ding slightly (5-10 points). Fact: Monitor monthly safely via MyCIBIL app.

- Myth: Cash Payments Ruin Score: Cash transactions invisible to CIBIL – only formal loans/cards reported. Fact: Build via credit products; cash good for habits but no direct boost.

- Myth: Women Receive Lower Scores: No gender bias; RBI mandates equality. Scores based on behavior alone. Fact: Marital status irrelevant; joint apps average scores.

Extra Common Ones

- Income directly affects score: False – repayment key.

- Closing cards improves score: Often worsens utilization.

Take Control of Your Credit Today

The persistent myth that a CIBIL score arrives automatically at 18 creates unnecessary delays for young Indians eager for independence. In reality, no credit history means no score, but turning 18 hands you the blueprint to architect a strong one. You’re not passive – become the master builder of your financial future.

Start modestly: Open that zero-balance account, snag an add-on card, dip into BNPL wisely. Prioritize on-time payments, cap utilization at 30%, and monitor reports religiously. Avoid pitfalls like over-applying or festival splurges. These habits compound: By 21, hit 700+ for job perks; by 25, 750+ unlocks personal loans; reach 30 with 800+ for dream homes or ventures.

Govt aids like PMJDY pave indirect paths. Consistency trumps speed – a stellar score by mid-20s flings open doors banks can’t shut, fueling cars, businesses, stability. Act now; your empowered tomorrow awaits.

Disclaimer: This analysis on Indian stock market trends is for educational and informational purposes only and does not constitute financial, investment, legal, tax, or accounting advice. Markets are volatile; past performance isn’t indicative of future results. Consult a qualified financial advisor before making investment decisions.